Posted: 8th April 2019

The FCA ended 2018 by publishing its key findings from the extensive work undertaken on pension transfer advice, another key publication in an ongoing series of work in the area that began all the way back in 2016.

The focus of this release was largely on those firms most active in the market, but also on firms that were brought to the FCA’s attention through whistleblowing. It’s interesting – but perhaps not surprising – that two of the 18 firms highlighted no longer operate in the market.

Before we look forward, it’s important to take stock and look back at some of the key market events from 2018.

2018 – A busy year for transfer advisors

It’s hard to ignore the scale of the Defined Benefit (DB) advice market, the FCA reporting that DB to DC (Defined Contribution) transfers rose in 2018 by 587% (as compared to March 2016).

According to the report, in the six months to March 2016, a total of 5,056 people transferred their pension, while in the six months to March 2018, 34,738 people transferred.

Interestingly, in 2018 there was a marked rise in the number of firms either voluntarily, or involuntarily (following FCA intervention), having had their pension transfer permissions removed. Many simply ceased operating entirely. Excluding firms involved in British Steel Pension Scheme (BSPS) advice scandal, it is reported that nine major firms were impacted in this way during 2018.

Defined Benefit Transfers – Still in demand?

It’s long been recognised that there are two main consumer drivers for the popularity of DB transfers, the primary driver being the high transfer value offered by DB schemes. The second appealing factor is being able to access all the money through ‘pension freedom options’ that are not offered through DB schemes.

The latter of these drivers is clearly here to stay for the foreseeable future, as it essentially hands responsibility back to consumers and opens up wider options for retirement provisions. The question is, though, will high transfer values continue being a popular factor in the same way? Well, that remains to be seen.

These values remain high, but have largely stabilised (read: are not increasing). However, as interest rates rise and pension scheme deficits fall, we may see these transfer values reducing in turn. This may make demand, certainly during 2019, weaker than it has been over the last few years.

Key FCA Findings

Let’s turn our attention back to the FCA findings published in December for a minute.

Regardless of whether you provide advice in this area or not, the findings from this report make for uncomfortable reading and don’t exactly paint the financial advice market in a pretty light.

The review collected information from an additional 45 firms, before conducting further assessment work, including file reviews and visits, on 18 of them. The FCA’s following report mainly focused on two areas:

Findings on suitability

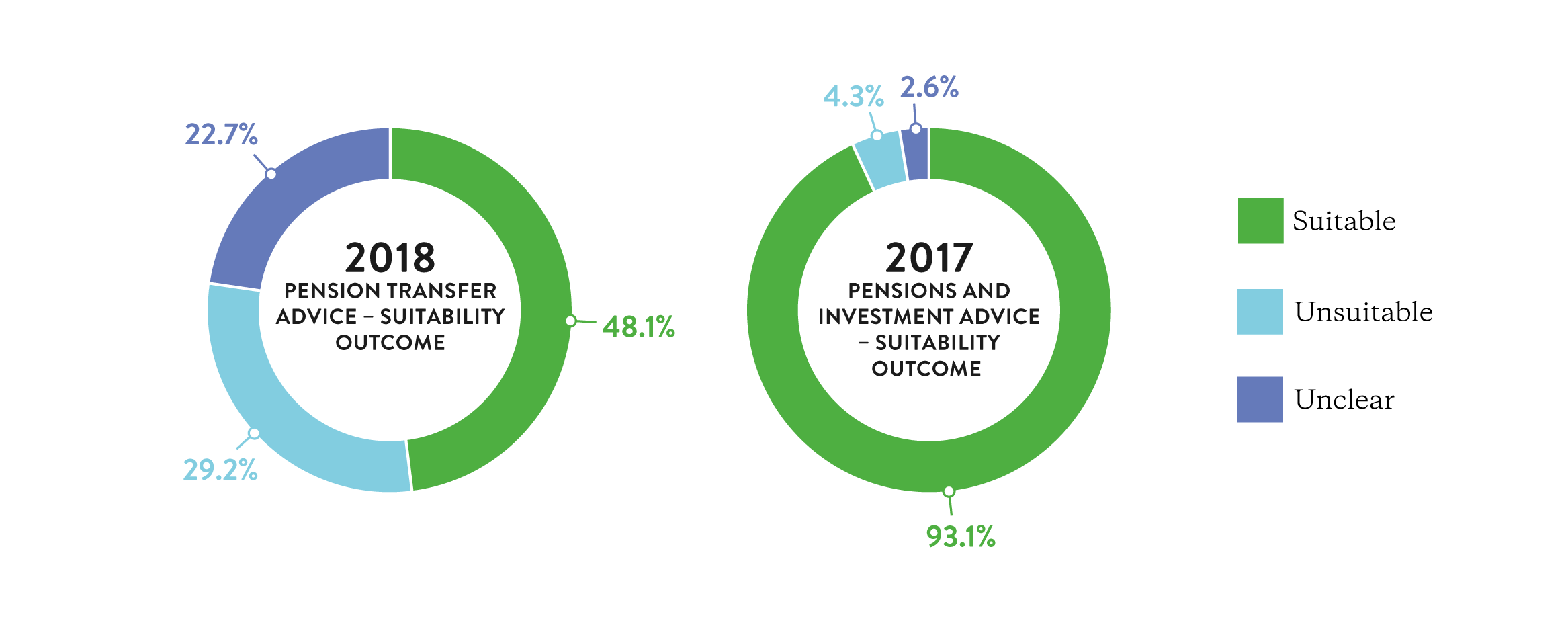

The review identified that the firms in question delivered suitable advice in only 48.1% of cases, unsuitable advice in 29.2% of cases, and unclear advice in 22.7% of cases. These are the highest “unsuitable” and “unclear” results of any suitability review undertaken by the FCA. The charts below highlight the stark contrast of the latest results compared to those in 2017 for pension and investment advice, for example. Clearly, there is a big problem here.

Alongside the data, the FCA also presents a list of firms’ failings. No reader of these would find it hard to spot the tone of frustration throughout, most evident whenever reference is made to the fact that these failings link all the way back to the October 2017 findings.

Firms have now been called out twice, in 2017 and again in 2018 for:

- Failing to obtain enough information about clients’ needs and personal circumstances

- Failing to consider the needs of the client alongside the client’s objectives when making a recommendation

- Not making an adequate assessment of the risk a client is willing and able to take in relation to their pension benefits

Findings on disclosure

The assessment of disclosure was also significant, with the FCA identifying that firms in the sector provided acceptable disclosure in only 29.2% of cases. In 61.7% of cases, non-compliant disclosure was provided. In 9.1% of cases, the sector provided unclear disclosure.

The review identified that most issues lay with firms’ levels of initial disclosure, including that relating to costs and charges. The primary issues were:

- The disclosure failings were driven in part by failings in firms’ standard documentation, particularly in the way they present initial and ongoing fees

- Misrepresentations about the scope of Pension Protection Fund protection

- Writing long suitability reports with unclear recommendations

- Firms did not present clear and fair information about the respective benefits and disadvantages of DB and Defined Contribution (DC) schemes

- Firms over-emphasised the benefits and downplayed the risks of transfer to an alternative arrangement

Moving forward in 2019

The results from the 2018 report highlight that, generally, only half of all customers received clear and suitable advice in relation to DB transfers, and just under a third of customers receive clear disclosure.

It stands to reason, then, that the FCA will not be letting up on their focus in this area. Identifying and addressing any harm caused by unsuitable advice will, more than likely, remain a key priority throughout 2019 and beyond.

Firms that operate in this market, therefore, must, as a priority, take on board all of the recommendations that have emerged from the FCA’s work. Specifically, where the FCA has published failings, firms will need to carry out internal healthchecks to identify whether the same – or similar – issues may exist within their own organisations.

Getting this right is not only crucial for customers now, but also for their futures. The impact advice plays in supporting them – or not – through retirement cannot be understated.

Richard Brown

Technical Advisor - Complaints

Related Content

Pensions

Regulatory update: CP19 / 25 – Pension transfer advice: contingent charging and other proposed changes

The FCA has proposed a ban on contingent charging within the pension transfer advice market – but will it deliver good outcomes?

Advice and suitability

Regulatory Update: Defined Benefit pension transfers – Market-wide data results

The FCA has released data from its market-wide investigation into DB pension transfer advice

General regulation

MiFID II Cost and Charges Disclosure – There are still challenges ahead

MiFID II may seem like old news, but there is still work to be done to ensure compliance across the sector

Customer Servicing

Delivering service excellence to your customers across the customer lifecycle